Terminating Employment During COVID-19

Firing an employee is never easy and is probably one of the most difficult decisions involved in running a business. However, in some situations, it may be a necessary step to take, especially when the employee’s performance is substandard or where, as here, unforeseen circumstances like the COVID-19 pandemic threaten the very existence of the business. This article covers the different “shades” of termination, and potential implications under the Consolidated Omnibus Budget Act (“COBRA”) and the recently enacted Coronavirus Aid, Relief, and Economic Security (“CARES”) Act.

When can I terminate an employee? Do I have to have "cause"?

Under Louisiana law, the default rule is that every employment relationship is “at will.” This means that the employment is terminable at the will of either party at any time. There are, however, some important exceptions. Termination cannot violate the constitutional rights of the employee or a specific statute. At-will employment can also be modified by a contractual agreement to work for a definite period of time. If such an agreement exists, then the employer must have “cause” to terminate the employment before the expiration of the term.

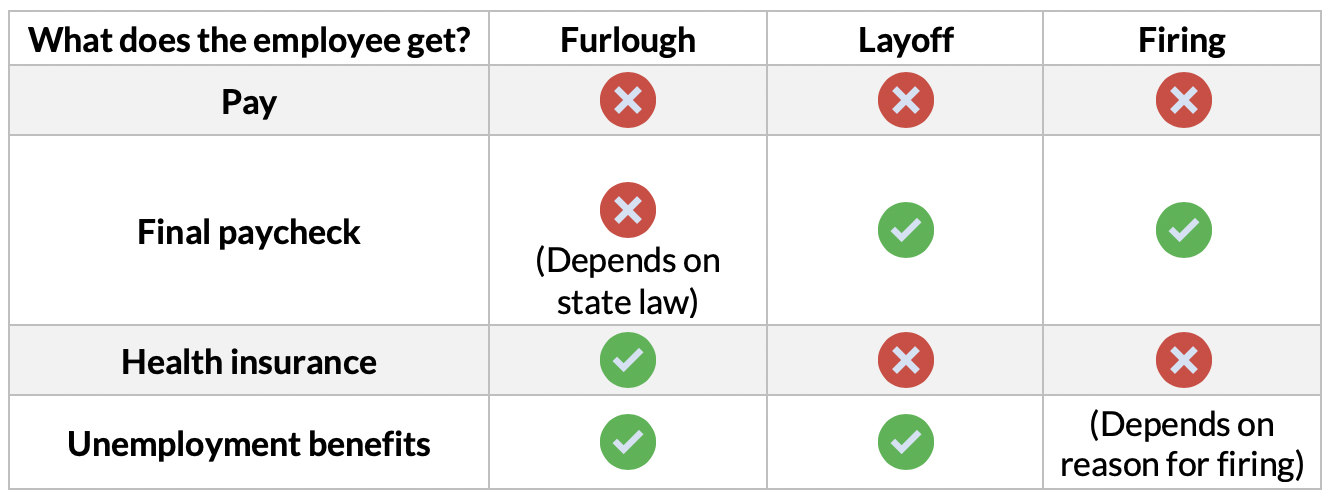

What’s the difference between a furlough vs. layoff vs. firing?

The terms “furlough,” “layoff,” and “firing” are often used interchangeably. But there are important differences between the three. Generally speaking, the first two categories—furloughs and layoffs—involve job losses where business finances or other outside factors, as opposed to employee performance, are the triggering factor. On the other hand, a firing generally occurs when a single employee is let go due to substandard or individual circumstances. In this sense, a firing is a true termination of the employment relationship.

But there are other distinctions, too. For instance, a furlough is generally for a shorter, fixed period of time, during which the employee remains on the company’s books as an employee. A layoff, on the other hand, is more akin to a firing, because it is normally an indefinite and permanent break in the employment relationship. Although a laid-off employee may be rehired, this is not always the case.

How does termination implicate COBRA?

The Consolidated Omnibus Budget Reconciliation Act (“COBRA”) gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances, such as voluntary or involuntary job loss, reduction in the hours worked, transition between jobs, death, divorce, and other life events. COBRA generally requires that group health plans sponsored by employers with 20 or more employees in the prior year offer employees and their families the opportunity for a temporary extension of health coverage (called “continuation coverage”) in certain instances where coverage under the plan would otherwise end. Thus, if a group health plan is covered by COBRA and a qualifying event occurs, such as termination of employment, then the terminated individual may be entitled to continuation coverage.

Who is entitled to continuation coverage under COBRA?

There are three requirements in order for an individual to be entitled to COBRA continuation coverage:

1. The individual’s group health plan must be covered by COBRA;

COBRA covers group health plans sponsored by an employer (private-sector or state/local government) that employed at least 20 employees on more than 50% of its typical business days in the previous calendar year. Both full- and part-time employees are counted to determine whether the 20-employee threshold is met, although part-time employees are counted as a fraction of a full-time employee.

2. A qualifying event must occur; and

The following are qualifying events for covered employees if they cause the covered employee to lose coverage:

a. Termination of the employee’s employment for any reason other than gross misconduct; or

b. Reduction in the number of hours of employment.

The following are qualifying events for the spouse and dependent child of a covered employee if they cause the spouse or dependent child to lose coverage:

c. Termination of the covered employee’s employment for any reason other than gross misconduct;

d. Reduction in the hours worked by the covered employee;

e. Covered employee becomes entitled to Medicare;

f. Divorce or legal separation of the spouse from the covered employee; or

g. Death of the covered employee.

The following is a qualifying event for a dependent child of a covered employee if it causes the child to lose coverage:

h. Loss of dependent child status under the plan rules.

3. The individual must be a qualified beneficiary or that event.

A qualified beneficiary is an individual covered by a group health plan on the day before a qualifying event occurred that caused him or her to lose coverage.

For more information on COBRA, please click here to visit the U.S. Department of Labor’s website.

How does termination implicate the CARES Act?

The Coronavirus Aid, Relief, and Economic Security (“CARES”) Act is a historic $2 trillion stimulus package that was recently enacted into law in response to the COVID-19 crisis. Among other things, the CARES act provides relief to American workers in the form of one-time direct payments, expanded unemployment insurance, suspended student loan payments, and more. And for small businesses, the CARES Act creates a new Small Business Administration loan program—the Paycheck Protection Program (“PPP”)—portions of which can be forgiven.

However, terminating an employee can have serious implications for on how much you’re eligible to receive under the PPP and, more importantly, how much you can have forgiven. Let’s start with the maximum amount of a PPP loan that an eligible borrower may receive. The maximum loan amount is the lesser of $10 million or a calculation involving payroll costs. Termination can impact the latter calculation, which requires you to calculate 250% of the average total monthly payments for payroll costs—which includes employee compensation—incurred during the one-year period before the date on which the loan is made. In other words, the amount is equal to the monthly average payroll costs for that period times 2.5. So, if you terminate one or more employees before the loan is disbursed, your average monthly payroll may decrease, which, in turn, may lower the amount of a PPP loan you’re eligible for.

Reductions in staffing may also impact the amount of a PPP loan that is eligible for forgiveness. Generally, the loan can be forgiven to the extent that it is used for payroll costs, interest on mortgage obligations incurred prior to February 15, 2020, rent payments for leases in force prior to February 15, 2020, and utility payments which began before February 15, 2020 during the eight-week period following the origination of the loan. This eight-week period following the origination of the loan is called the “covered period.” However, the amount forgiven is reduced by multiplying the loan forgiveness amount by a fraction:

- The numerator of which is the average number of full-time employees per month employed during the covered period; and

- The denominator of which is the average number of full-time employee equivalents employed from February 15, 2019 through June 30, 2019 or January 1, 2020 through February 29, 2020 (the employer can elect which time period to use).

For example, assume your business receives a $1 million PPP loan. During either of the two time periods stated above, your business employed an average of 100 full-time employee equivalents. However, during the covered period, the number of full-time employee equivalents decreased to 75. The amount of loan forgiveness would decease to $750,000, because three-fourths (75/100) of $1 million is $750,000. This is also assuming that the entire $1 million loan is used for permitted and forgivable purposes.

While layoffs may be a temporary solution in dealing with the COVID-19 crisis, it is important to keep in mind the potential relief under the CARES Act, which may be negatively impacted by employee layoffs or terminations.

For more information on the CARES Act and PPP loans, click here.